Debt is a sneaky adversary. It rarely takes over your financial life overnight. Instead, it creeps in slowly—a car loan here, a credit card balance carried over there, a “buy now, pay later” purchase you couldn’t resist. Because borrowing money has become completely normalized in modern society, it is incredibly easy to convince yourself that carrying a heavy debt load is just a standard part of adulthood.

But there is a massive difference between strategically using debt to buy an appreciating asset (like a home) and drowning in consumer debt that silently eats away at your future wealth.

Here at Wealth Path Daily, we believe that true financial freedom begins the moment you stop paying interest to banks and start paying yourself. If you are tossing and turning at night worrying about your finances, it is time to take a hard, objective look at your situation.

Are you simply managing normal liabilities, or are you dangerously over-leveraged? Here are five glaring warning signs that you have too much debt, and exactly how you can course correct before it is too late.

The 5 Warning Signs You Are Drowning in Debt

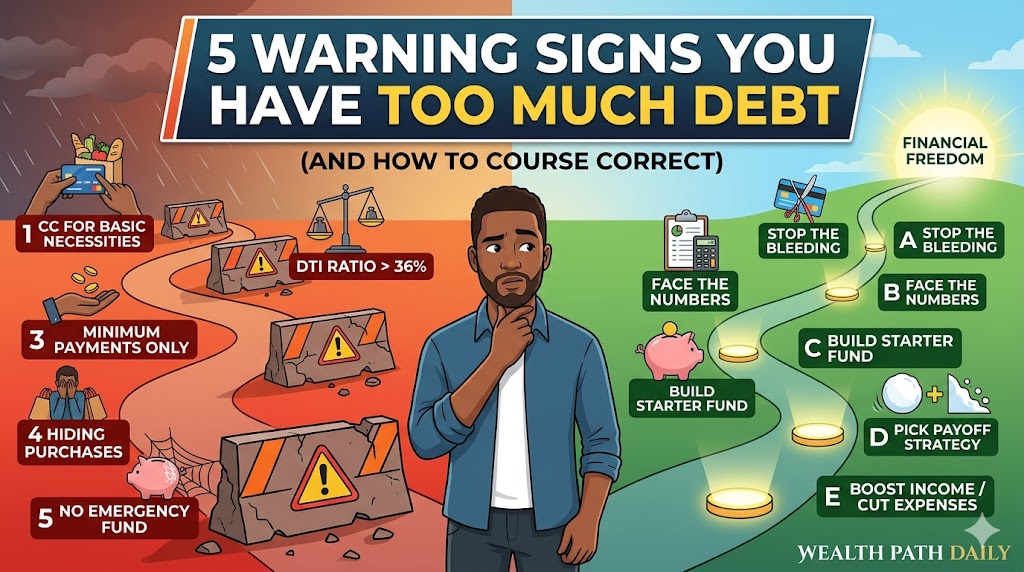

1. You Are Relying on Credit Cards for Basic Necessities

Credit cards can be fantastic tools for earning travel rewards or cash back—but only if you are paying the statement balance in full every single month. If you have reached a point where your paycheck runs out before the end of the month, and you are forced to swipe a credit card just to buy groceries, put gas in your car, or pay the electric bill, you are in the danger zone. This is a massive red flag that your lifestyle costs more than your income can support, creating a cycle of reliance that compounding interest will quickly turn into a nightmare.

2. Your Debt-to-Income (DTI) Ratio Exceeds 36%

Numbers do not lie. Lenders use a specific mathematical formula to determine if you have too much debt, and you should use it too. It is called your Debt-to-Income (DTI) ratio.

To calculate it, add up all your minimum monthly debt payments (rent/mortgage, auto loans, credit cards, student loans). Then, divide that number by your gross monthly income (your income before taxes). If the resulting percentage is above 36%, you are carrying too much debt. If it is over 43%, you are severely over-leveraged, and a single financial emergency could push you into default.

3. You Are Only Making the Minimum Payments

When you get your credit card statement, the bank helpfully highlights a “Minimum Payment Due.” This number is designed to keep you in debt for as long as legally possible. If you are consistently only paying the minimums on your credit cards, nearly all of your money is going toward interest charges, not the actual principal balance. At 24% interest, making only minimum payments means a $5,000 balance could take over a decade to pay off and cost you thousands of dollars in extra fees.

4. You Are Hiding Purchases or Experiencing “Debt Shame”

Debt is not just a math problem; it is a profound psychological burden. If you find yourself hiding shopping bags in the trunk of your car, lying to your spouse about how much you owe, or feeling a pit of anxiety in your stomach every time the mail arrives, your debt has crossed the line from a financial tool to a source of trauma. Financial infidelity and avoidance are clear behavioral indicators that your debt is out of control.

5. You Have No Emergency Fund

When your monthly debt payments consume a massive portion of your paycheck, there is nothing left over to save. If you do not have at least $1,000 to $3,000 sitting in a high-yield savings account for emergencies, you are walking a financial tightrope without a net. Without an emergency fund, the next time your car breaks down or your water heater bursts, you will be forced to put that expense on a credit card, digging the hole even deeper.

How to Course Correct: Your Actionable Rescue Plan

If you recognized yourself in any of the warning signs above, take a deep breath. Do not panic, and do not let shame paralyze you. You can fix this. Follow this actionable, step-by-step rescue plan to regain control of your financial life:

- Step 1: Stop the Bleeding. You cannot dig yourself out of a hole while you are still holding a shovel. Take your credit cards out of your wallet, delete them from your phone’s digital wallet, and remove the saved numbers from your favorite online stores. Commit to a cash-only or debit-only lifestyle until the debt is cleared.

- Step 2: Face the Numbers. Sit down with a pen and paper. Write out every single debt you owe, the total balance, the minimum monthly payment, and the interest rate. You must know exactly what you are up against.

- Step 3: Build a Starter Emergency Fund. Before you aggressively attack the debt, save a $1,000 “starter” emergency fund. This will act as a buffer so that a minor inconvenience doesn’t force you to use your credit cards again.

- Step 4: Pick a Payoff Strategy. Choose between the Debt Snowball (paying off the smallest balance first for quick psychological wins) or the Debt Avalanche (paying off the debt with the highest interest rate first to save the most money). Both work; pick the one that keeps you motivated.

- Step 5: Ruthlessly Cut Expenses and Boost Income. To accelerate your payoff, you need a larger gap between your income and your expenses. Cancel unused subscriptions, stop eating out temporarily, and consider picking up a side hustle or selling unwanted items around your house. Direct 100% of this extra cash flow directly at your debt.

Conclusion

Carrying a heavy burden of debt robs you of your peace of mind and steals from your future wealth. Acknowledging that you have a problem is the hardest, yet most crucial, part of the journey.

If you are displaying the warning signs of too much debt, realize that today is the perfect day to draw a line in the sand. By confronting your numbers, cutting up your cards, and executing a ruthless payoff strategy, you can break the chains of compounding interest. It will require discipline and short-term sacrifice, but the feeling of keeping 100% of your paycheck is worth every ounce of effort.

Stay tuned to Wealth Path Daily for more actionable personal finance strategies designed to help you build a richer, more intentional life.