Managing your own money is an empowering journey. For years, you might do perfectly fine following the core principles we discuss here at Wealth Path Daily: automating your index fund investments, maintaining a strict budget, and aggressively paying down high-interest debt.

But as your net worth grows, your financial picture inevitably becomes more complex.

Perhaps you have started a profitable side business, received an inheritance, or are finally staring down the barrel of retirement. Suddenly, a simple DIY spreadsheet isn’t quite enough to optimize your tax strategy, plan your estate, or protect your accumulated wealth. It might be time to bring in a professional.

However, the financial services industry is famously murky. Handing over the keys to your life’s savings is one of the most significant decisions you will ever make, and choosing the wrong person can cost you hundreds of thousands of dollars in hidden fees and poor advice.

If you are ready to scale your financial team, here is your comprehensive guide to choosing the right financial advisor—and the massive red flags you must avoid at all costs.

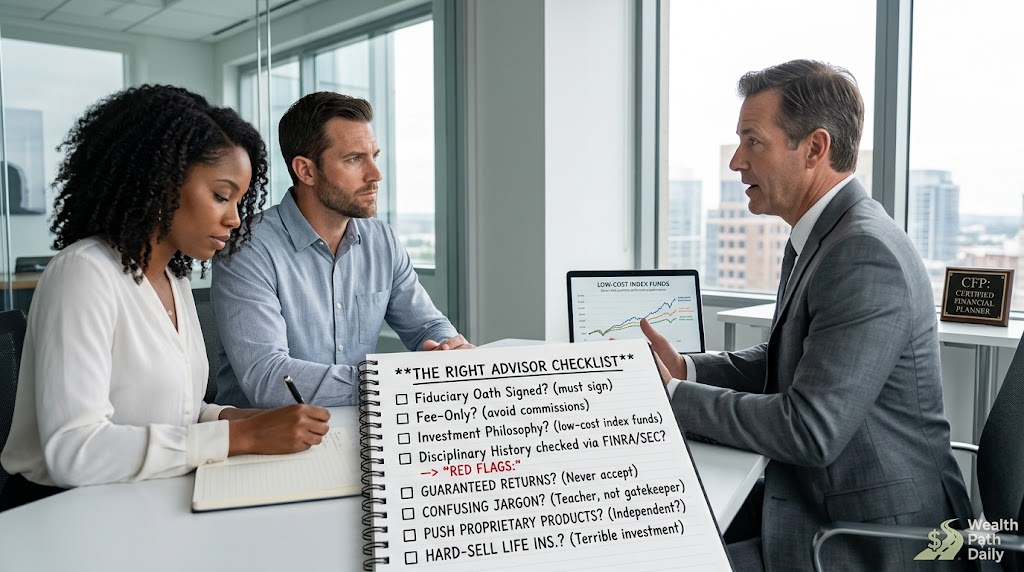

The Golden Rule: Only Hire a Fiduciary

If you only take one piece of advice from this article, let it be this: You must only hire a fiduciary. In the financial world, professionals are generally held to one of two legal standards:

1. The Suitability Standard

Many brokers and insurance agents operate under the “suitability standard.” This means that any product they recommend to you must simply be “suitable” for your age, income, and risk tolerance. It does not mean it has to be the best product available. If there are two identical mutual funds, and one pays the advisor a massive commission while the other is cheaper for you, an advisor under the suitability standard is legally allowed to sell you the expensive one.

2. The Fiduciary Standard

A fiduciary is legally and ethically bound to act in your absolute best financial interest, even if it means they make less money. They must eliminate or disclose all conflicts of interest. When you hire a fiduciary, you are hiring a financial partner whose success is directly aligned with your own.

Actionable Tip: Do not just take their word for it. Ask them to sign a “Fiduciary Oath” document stating they will act as your fiduciary 100% of the time.

Understanding How Advisors Get Paid

You can tell exactly who a financial advisor truly works for by looking at how they get paid. There are three main compensation models in the industry:

- Commission-Based: These advisors are essentially salespeople. They earn money when they sell you specific financial products, like annuities, loaded mutual funds, or whole life insurance policies. This creates a massive conflict of interest.

- Fee-Based: This is deliberately confusing. “Fee-based” means they charge you a flat fee for their advice, but they can also earn commissions on the back end by selling you certain products. They can switch their fiduciary hat on and off.

- Fee-Only: This is the gold standard. A fee-only advisor only gets paid directly by you. They do not accept kickbacks, commissions, or referral fees from mutual fund companies. They usually charge an hourly rate, a flat annual retainer, or a percentage of the Assets Under Management (AUM)—typically around 1%.

For the vast majority of investors, a Fee-Only Fiduciary is the only type of advisor you should consider hiring.

5 Glaring Red Flags to Avoid

When you are interviewing prospective advisors, keep your guard up. If you spot any of these five red flags, politely end the meeting and walk away:

1. They Guarantee Specific Returns

The stock market is inherently unpredictable. If an advisor promises that they can consistently “beat the market” or guarantees a specific percentage return on your investments, they are either lying or engaging in incredibly reckless strategies. A true professional focuses on managing risk and asset allocation, not predicting the future.

2. They Use Confusing Jargon to Intimidate You

Your advisor should be a teacher, not a gatekeeper. If you ask a simple question about where your money is going and they respond with a five-minute monologue filled with acronyms and complex jargon, they are trying to make you feel financially illiterate so you surrender control. If you don’t understand an investment, never put your money into it.

3. They Push Proprietary Products

If an advisor works for a massive bank or brokerage and strictly recommends mutual funds created by that exact same bank, run. They are acting as a corporate salesperson, not an independent advisor.

4. They Hard-Sell Permanent Life Insurance

While whole life or indexed universal life insurance can have a place in incredibly complex, ultra-high-net-worth estate planning, it is generally a terrible investment for the average person. These policies carry massive hidden fees and pay enormous commissions to the advisor selling them. If this is the first thing they pitch you, they are looking at you as a payday.

5. They Have a Disciplinary History

Never hire someone without running a background check. You can use the free BrokerCheck tool provided by FINRA (the Financial Industry Regulatory Authority) or the SEC’s Investment Adviser Public Disclosure (IAPD) website. If they have a long history of customer disputes or regulatory fines, cross them off your list immediately.

Your Actionable Interview Checklist

Finding the right advisor is like hiring a key executive for the business of your life. You should interview at least three candidates before making a decision. Bring this checklist of questions to your initial meetings:

- “Are you a fiduciary 100% of the time, and will you put that in writing?” (If they hesitate, leave.)

- “How exactly do you get paid? Please list every fee I will incur.”

- “What is your investment philosophy?” (Look for passive, low-cost index investing rather than active, high-frequency trading.)

- “Who is your typical client?” (You want an advisor who regularly works with people in your specific financial bracket and life stage.)

- “Where will my money be held?” (Your money should always be held by an independent third-party custodian—like Charles Schwab or Fidelity—never directly by the advisor’s firm. This prevents Ponzi schemes.)

Conclusion

Handing over the management of your Wealth Path is a massive milestone, and it deserves to be treated with rigorous scrutiny. You worked incredibly hard to build your net worth; do not let it be eroded by hidden fees, poor advice, or greedy salespeople masquerading as financial planners.

By insisting on a fee-only fiduciary, understanding the payment models, and confidently interviewing your candidates, you can find a brilliant financial partner who will help you protect your assets, minimize your taxes, and secure your family’s future for decades to come.

Stay tuned to Wealth Path Daily for more actionable personal finance strategies designed to help you build a richer, more intentional life.