You have finally decided to take control of your financial future. You have paid down your high-interest debt, built an emergency fund, and opened a brokerage account. You are ready to start investing. But the moment you log in, you are hit with a tidal wave of financial jargon, ticker symbols, and endless investment options.

If you are feeling overwhelmed, take a deep breath. You are not alone.

Here at Wealth Path Daily, we believe that investing shouldn’t require a Wall Street pedigree. For decades, the financial industry has intentionally made investing seem overly complicated to justify high fees. But the truth is, the most successful long-term investment strategies are often the simplest.

As a beginner, you will inevitably run into the two heavyweights of the investing world: Mutual Funds and Index Funds. Both allow you to buy a basket of stocks with a single purchase, but they operate on fundamentally different philosophies.

Which one should you choose? Let’s break down the differences, look at the math, and declare a clear winner for beginner investors.

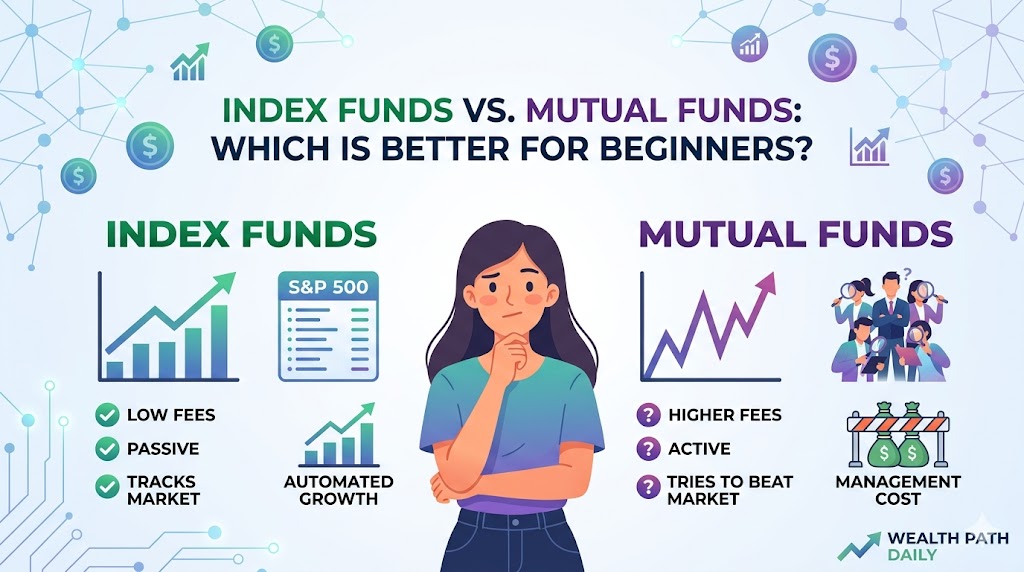

What is a Mutual Fund? (The Active Approach)

When most people say “mutual fund,” they are referring to an actively managed mutual fund.

Think of an actively managed mutual fund as hiring a high-priced chauffeur. You pool your money together with thousands of other investors, and hand it over to a professional fund manager and their team of analysts. This team constantly buys and sells individual stocks within the fund.

The Goal: The primary objective of an active mutual fund manager is to “beat the market.” They are trying to pick the winning stocks and avoid the losers to generate a higher return than the overall stock market.

What is an Index Fund? (The Passive Approach)

An index fund is actually a type of mutual fund (or Exchange Traded Fund), but it strips away the high-priced managers.

Instead of paying a team of analysts to guess which stocks will perform best, an index fund simply tracks a specific market index. The most famous example is the S&P 500, which represents the 500 largest publicly traded companies in the United States (think Apple, Microsoft, Amazon, etc.). If you buy an S&P 500 index fund, you are automatically buying a tiny slice of all 500 companies.

The Goal: An index fund does not try to beat the market; it simply aims to match the market. It is a passive, “set it and forget it” approach.

The Great Debate: Head-to-Head Comparison

To determine which is better for your portfolio, we need to compare them across three critical categories: Cost, Performance, and Simplicity.

1. Cost and Fees (Expense Ratios)

Every fund charges an annual fee, known as an Expense Ratio. This is where index funds completely crush actively managed mutual funds.

Because active mutual funds have to pay the salaries of their hotshot managers and research teams, their fees are high. A typical active mutual fund might charge an expense ratio of 1.0% or more. That means if you invest $10,000, you pay $100 every year in fees, regardless of whether the fund makes or loses money.

Index funds are run by computer algorithms, not expensive humans. Therefore, their fees are incredibly low. A standard S&P 500 index fund might charge an expense ratio of just 0.03%. On that same $10,000 investment, you are paying a mere $3 a year.

Over a 30-year investing timeline, a 1% difference in fees can literally eat up hundreds of thousands of dollars of your potential wealth.

2. Performance

You might be thinking, “I don’t mind paying a 1% fee if the active manager is beating the market!” That is a fair point—except they rarely do.

Year after year, data proves that humans are terrible at predicting the stock market. According to the S&P Indices Versus Active (SPIVA) scorecard, over a 15-year period, nearly 90% of actively managed mutual funds underperform their benchmark index.

In other words, by paying high fees for a professional manager, you are statistically guaranteeing that you will make less money than if you had simply bought a passive index fund.

3. Simplicity and Stress

Active mutual funds often have high minimum investment requirements (sometimes $3,000 or more) and can generate unexpected capital gains taxes if the manager is frequently buying and selling stocks.

Index funds are incredibly tax-efficient because they rarely buy and sell. Furthermore, many brokerages allow you to buy fractional shares of index funds, meaning you can start investing with as little as $1.

Actionable Tips for Beginner Investors

Ready to put this knowledge into practice? Here is an actionable checklist to help you get started with your first index fund investment:

- Open a low-cost brokerage account: Look for established, reputable brokers that offer zero-commission trading (e.g., Fidelity, Vanguard, or Charles Schwab).

- Identify your account type: Are you investing for retirement? Consider a Roth IRA. Are you investing for a shorter-term goal? A standard taxable brokerage account might be best.

- Choose a broad-market index fund: Look for funds that track the S&P 500 or the Total Stock Market. Check the “Expense Ratio” to ensure it is below 0.10%.

- Automate your investments: Set up an automatic transfer from your checking account to your brokerage account every time you get paid.

- Ignore the news: The stock market will go up and down. Do not panic-sell when the market drops. Keep investing consistently and let compound interest do the heavy lifting over the next few decades.

Conclusion: The Winner is Clear

For the vast majority of investors—especially beginners—Index Funds are the undisputed winner. They offer significantly lower fees, better long-term performance, and incredible simplicity. Investing doesn’t have to be a full-time job. By choosing low-cost index funds, you are taking a massive step toward financial independence, allowing you to spend less time worrying about your portfolio and more time actually living your life.

Stay tuned to Wealth Path Daily for more actionable personal finance strategies designed to help you build a richer, more intentional life.