If you are currently trapped in the suffocating cycle of high-interest credit card debt, you know exactly how desperate the desire for a clean slate can feel. When you are paying 20% to 25% in annual interest, every monthly payment feels like a drop in the ocean.

Then, you log into your retirement account. You see a healthy 401(k) balance sitting right there, doing its thing in the background. The thought inevitably crosses your mind: “Why am I paying a massive bank 24% interest when I have my own money just sitting right there? Shouldn’t I just borrow from myself?”

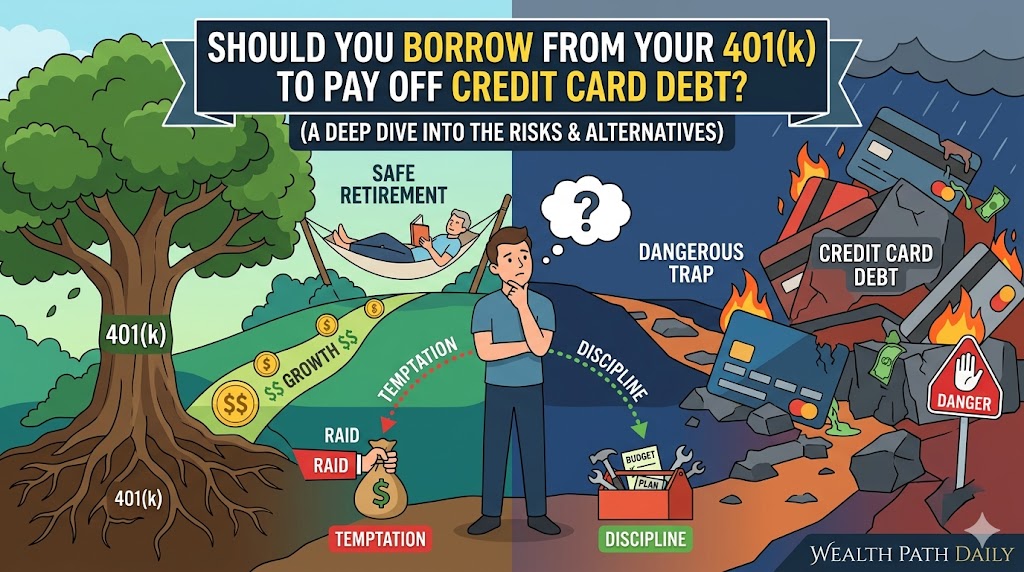

It is one of the most common, tempting, and dangerous questions in personal finance.

Here at Wealth Path Daily, our mission is to help you build long-lasting, generational wealth. We understand the intense psychological pressure of debt, but we also know that short-term relief can sometimes cause permanent long-term damage.

Before you click “submit” on that 401(k) loan application, you need to understand exactly what you are risking. Here is the definitive guide on whether you should raid your retirement to pay off your credit cards.

How a 401(k) Loan Actually Works

Unlike a standard withdrawal (which permanently removes the money and triggers massive taxes and penalties), a 401(k) loan allows you to borrow a portion of your vested balance—usually up to 50% or $50,000, whichever is less.

You must repay the loan, with interest, over a set period (usually five years) through automatic payroll deductions.

On paper, the marketing pitch sounds flawless: there is no credit check, the interest rate is usually much lower than a credit card (typically the Prime Rate plus 1% or 2%), and the best part is that the interest you pay goes directly back into your own 401(k) account.

If you are paying yourself the interest, it’s a win-win, right? Not exactly.

The Hidden Dangers: Why It is Usually a Terrible Idea

While a 401(k) loan looks like a mathematical lifeline, it is riddled with hidden traps that can permanently cripple your financial future.

1. The Massive Opportunity Cost

This is the biggest wealth-killer of a 401(k) loan. When you borrow $10,000 from your retirement account, you have to literally sell $10,000 worth of your investments. That money is no longer in the stock market.

If the market goes on a massive bull run while your money is sitting in your checking account paying off credit cards, you miss out on all of that compound growth. Yes, you are paying yourself 8% interest, but you might be missing out on a 15% to 20% market return. Over a 20-year timeline, missing out on just a few years of compound interest can cost you tens of thousands of dollars in retirement.

2. The “Job Loss” Trap

When you take a 401(k) loan, you are anchoring yourself to your current employer. If you quit, get laid off, or are fired, the loan rules change dramatically.

Under current IRS rules, if you leave your job, the outstanding balance of your 401(k) loan is typically due by the tax filing deadline of the following year. If you cannot pay the full balance back in cash, the loan defaults. It is then treated as an “early distribution.” You will owe income taxes on the entire balance, plus a massive 10% early withdrawal penalty to the IRS.

3. The Double Taxation Flaw

Remember how you are “paying yourself interest”? There is a catch. You repay a 401(k) loan using after-tax dollars from your paycheck. However, when you eventually retire and withdraw that money, it will be taxed again as standard income. You are voluntarily choosing to be taxed twice on the same money.

4. The Behavioral Illusion

A 401(k) loan treats the symptom (the balance) without curing the disease (your spending habits). Many people use their retirement funds to wipe their credit cards clean, experience a massive rush of relief, and then immediately start using the credit cards again because their core financial habits haven’t changed. Within a year, they have a 401(k) loan and maxed-out credit cards.

When Is a 401(k) Loan Acceptable?

In personal finance, there are very few absolute “nevers.” A 401(k) loan should be viewed as a last-resort emergency parachute, not a strategic financial tool.

You should only consider it if:

- You are facing immediate bankruptcy, foreclosure, or eviction.

- You have a massive, life-threatening medical emergency.

- You have exhausted absolutely every other available option.

Using it simply to erase consumer debt that you acquired through lifestyle inflation is a misuse of the tool.

Actionable Alternatives to Raiding Your Retirement

Before you sacrifice your future security, aggressively pursue these alternatives to crush your credit card debt:

- Open a 0% APR Balance Transfer Card: If your credit score is still decent, transfer your high-interest debt to a 0% promotional card. This gives you 12 to 21 months to pay down the principal without paying a dime in interest, and it leaves your 401(k) untouched.

- Explore a Debt Consolidation Loan: Consider taking out a personal unsecured loan from a local credit union. The interest rate will be higher than a 401(k) loan, but much lower than a credit card, and it does not put your retirement assets at risk.

- Pause 401(k) Contributions Temporarily: Instead of borrowing from the account, temporarily stop contributing new money to your 401(k) (unless you are getting an employer match). Redirect that monthly cash flow strictly toward your credit cards.

- Embrace the Debt Avalanche: Rank your debts from highest interest rate to lowest. Pay the minimum on everything, and throw every spare penny—from side hustles, selling household items, or cutting your budget to the bone—at the highest interest card until it is gone.

Conclusion

Your 401(k) is a vault designed for one specific purpose: ensuring you do not run out of money when you are too old to work. It is not a piggy bank, and it is not a bailout fund for past financial mistakes.

Borrowing from your 401(k) to pay off credit cards replaces one type of risk with a much more dangerous one. It jeopardizes your compound growth, ties you to your employer, and triggers severe tax penalties if things go wrong. Keep your retirement money where it belongs—in the market, growing quietly—and use the power of a strict budget and disciplined debt payoff strategies to clear your credit cards once and for all.

Stay tuned to Wealth Path Daily for more actionable personal finance strategies designed to help you build a richer, more intentional life.