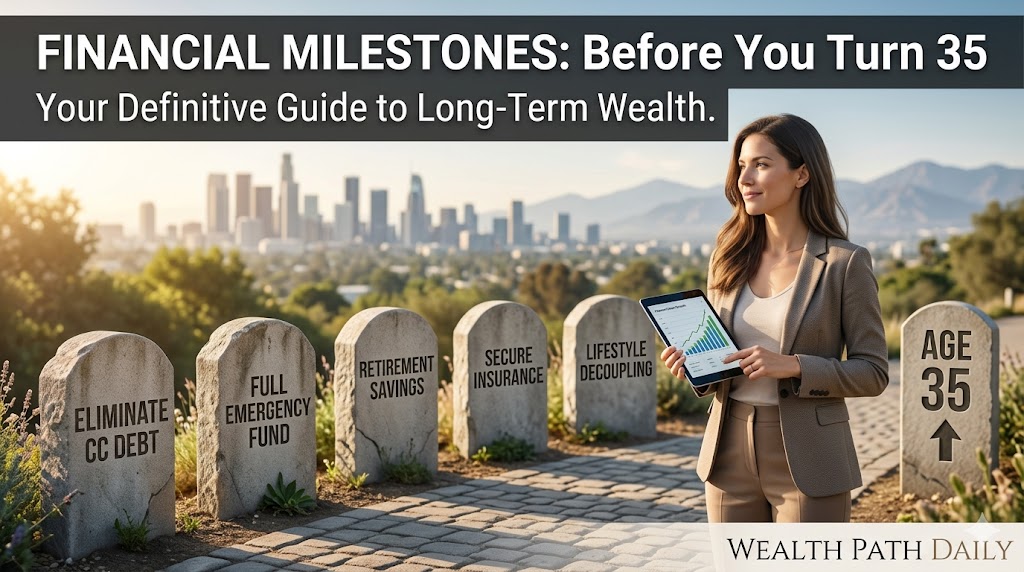

The Ultimate Checklist: Financial Milestones You Should Aim to Hit Before Turning 40

Turning 40 is a profound psychological and financial pivot point. You are officially transitioning out of your “early career” phase—where you were likely focused on finding your footing, learning your industry, and perhaps making a few expensive financial mistakes. You are now entering your peak earning years.

By the time you blow out the candles on your 40th birthday, the runway between you and retirement is no longer an abstract, distant concept; it is a measurable timeline. The decisions you make in this decade will heavily dictate the quality of your life in your 60s and beyond.

Here at Wealth Path Daily, we believe that wealth is not about luck; it is about building scalable, sustainable systems. While everyone’s financial journey is completely unique, having a benchmark gives you a target to aim for. If you are navigating your 30s and want to ensure you are setting yourself up for long-term financial independence, here are the five crucial financial milestones you should aim to hit before turning 40.

Milestone 1: Eradicate All High-Interest Consumer Debt

In your 20s, a bit of credit card debt or a hefty student loan might have felt like a normal rite of passage. By 40, carrying high-interest debt is a massive roadblock to wealth accumulation.

The Cost of Carrying Debt into Your 40s

When you are paying 20% to 25% interest on credit cards, you are essentially trying to sprint while wearing a lead vest. You cannot successfully leverage compound interest in your investment accounts if you are simultaneously paying exorbitant compound interest to a bank. Before you reach 40, your goal should be to completely eliminate all credit card balances, personal loans, and high-interest vehicle loans.

Note: A reasonable mortgage or a low-interest student loan is acceptable, but toxic consumer debt must be eradicated.

Milestone 2: Build a Fully-Funded, “Ironclad” Emergency Fund

When you are 25, a $1,000 starter emergency fund might be enough to cover a flat tire. By the time you are 40, your life is likely much more complex. You might have a mortgage, dependents, aging parents, or a senior-level career that would take longer to replace if you were laid off.

Before 40, you need to transition from a “starter” fund to an “ironclad” emergency fund. This means having three to six months of absolute baseline living expenses parked in a high-yield savings account (HYSA). If you are a freelancer or a business owner with irregular income, that number should comfortably stretch to nine or twelve months. This money is your ultimate sleep-at-night insurance.

Milestone 3: Accumulate 3x Your Salary in Retirement Savings

This is the milestone that often causes the most panic, but it is a critical benchmark. Major financial institutions, such as Fidelity, generally recommend that you should have three times your annual salary saved for retirement by age 40. If you make $80,000 a year, your target retirement portfolio across your 401(k), IRAs, and taxable brokerage accounts should be roughly $240,000.

Why This Multiplier Matters

This milestone is less about the exact dollar amount and more about the momentum of compound interest. If you can hit this 3x multiplier by 40, the math works beautifully in your favor. Even if you never increased your contribution rate again, the compounding growth of that nest egg over the next 25 years will likely carry you to a multi-million dollar retirement. If you are behind on this metric, your late 30s are the time to aggressively increase your contribution percentages.

Milestone 4: Secure Your Defensive Perimeter (Insurance & Estate)

Wealth building is about offense, but wealth preservation is about defense. By 40, you are no longer just responsible for yourself. If something catastrophic were to happen to you, would your family be financially ruined?

Hitting 40 means your financial defense must be impenetrable:

- Term Life Insurance: If anyone relies on your income, you need a term life insurance policy (usually 10x to 15x your annual salary). Avoid expensive whole-life policies; buy term and invest the difference.

- Disability Insurance: Your ability to earn an income is your most valuable asset. Ensure you have long-term disability coverage.

- A Basic Estate Plan: You must have a legally binding Will, designated account beneficiaries, and a healthcare directive. This is non-negotiable by age 40.

Milestone 5: Decouple Your Lifestyle from Your Income

The most dangerous financial trap of your 30s is “lifestyle creep”—the phenomenon where your spending increases at the exact same rate as your salary. You get a $10,000 raise, and suddenly you upgrade your car, buy a nicer wardrobe, and take more expensive vacations, leaving your actual savings rate exactly where it was.

By 40, you should have mastered the art of decoupling your lifestyle from your income. This means intentionally creating a massive gap between what you earn and what you spend.

Actionable Steps to Accelerate Your Progress

If you are looking at this list and feeling behind, do not panic. You have time, but you must take intentional action. Here is an actionable checklist to accelerate your Wealth Path today:

- Automate Your Escalation: Log into your 401(k) or investment portal today and set your contributions to automatically increase by 1% or 2% every single year. You won’t miss the small deduction, but it will dramatically compound over the decade.

- Audit Your Subscriptions: Go through the last 90 days of your bank statements. Cancel every single recurring charge, membership, or subscription you do not actively use. Redirect that money instantly to your debt payoff or emergency fund.

- Bank Your Raises: Commit to a new rule: Every time you get a raise or a bonus at work, immediately allocate 50% of the new money to investments or debt, and allow yourself to use the remaining 50% for lifestyle upgrades.

- Create a “Debt Avalanche”: List all your debts from highest interest rate to lowest. Pay the minimums on everything, and ruthlessly attack the one with the highest rate until it is gone.

Conclusion

Hitting these financial milestones before 40 does not require a massive inheritance or a six-figure tech salary. It requires discipline, automation, and the willingness to make strategic, sometimes uncomfortable choices in your 30s.

Remember, these milestones are not pass/fail grades; they are compass headings. Even if you don’t hit the exact target by the time you turn 40, aggressively aiming for them will fundamentally transform your financial trajectory. Take control of your numbers today, so you can enjoy the freedom and flexibility you deserve in the decades to come.

Stay tuned to Wealth Path Daily for more actionable personal finance strategies designed to help you build a richer, more intentional life.