Have you ever reached the end of the month, checked your bank account, and thought, “Where did all my money go?” If you feel like you earn a decent living but still struggle to gain traction on your financial goals, you are not alone. Millions of people fall into the trap of passive money management—spending what is in their checking account until the next payday, hoping for the best.

But hope is not a financial strategy. Here at Wealth Path Daily, we believe that true financial freedom starts with intention. And there is no better tool for intentional wealth-building than the zero-based budget.

In this guide, we are going to break down exactly what a zero-based budget is, why it is so remarkably effective, and how you can implement it to finally take control of your financial future.

What is a Zero-Based Budget?

At its core, a zero-based budget is based on a simple mathematical formula:

Income – Expenses = Zero

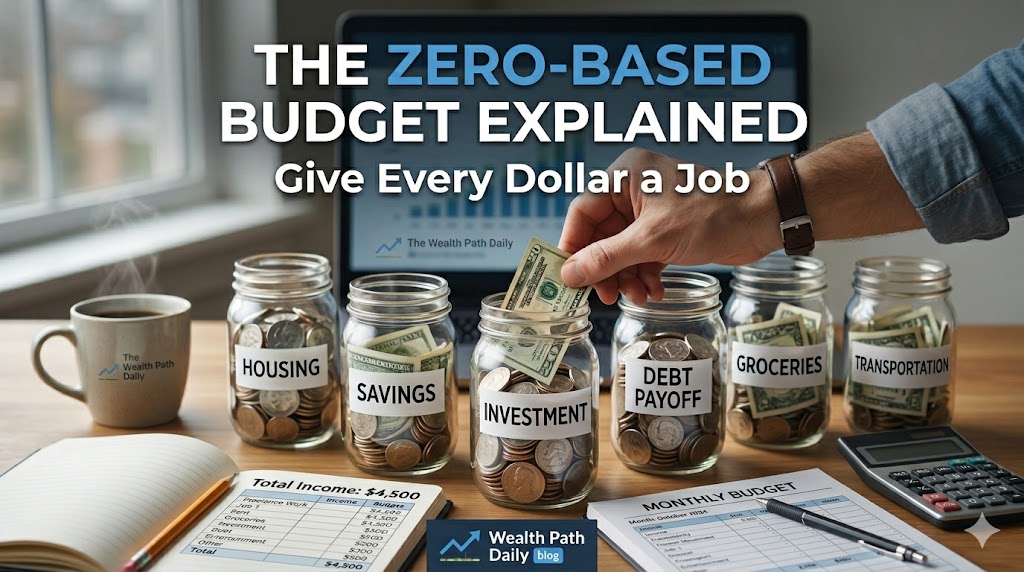

When you hear “zero,” do not panic. This does not mean your bank account balance drops to zero at the end of the month. It means that your unassigned income drops to zero. In other words, you are giving every single dollar a specific job before the month even begins.

Whether a dollar’s job is to pay the mortgage, buy groceries, fund your emergency savings, or pay down high-interest credit card debt, it must have a designated purpose. If you earn $5,000 a month, you must assign exactly $5,000 to various categories. Leaving $300 sitting in your account “just in case” defeats the purpose, because unassigned money is almost always wasted money.

Traditional Budgeting vs. Zero-Based Budgeting

Traditional budgeting often involves looking at your past spending, setting rough limits for the future, and trying to stay under them. If you have money left over, great! But often, that leftover money evaporates into impulse purchases or lifestyle creep.

Zero-based budgeting flips the script. Instead of looking backward, it looks forward. It demands that you are proactive rather than reactive, forcing you to align your spending exactly with your current financial goals.

How to Create a Zero-Based Budget in 4 Simple Steps

Starting a zero-based budget might feel intimidating, but the process is highly logical. Here is how to build yours from the ground up:

1. Calculate Your Total Monthly Income

Before you can assign jobs to your dollars, you need to know exactly how many dollars you have to work with. If you are a salaried employee, this is as simple as looking at your net pay (your after-tax income).

If you are a freelancer, gig worker, or have variable income, use a conservative estimate based on your lowest-earning month from the past year. Do not forget to include side hustles, child support, or dividend income.

2. List All of Your Expenses

Write down every single thing you spend money on in a typical month. It helps to break these down into a clear hierarchy:

- The Four Walls: Housing, utilities, basic groceries, and basic transportation. These are non-negotiable survival expenses.

- Obligations: Minimum debt payments, insurance premiums, and child care.

- Variable Expenses: Dining out, entertainment, streaming subscriptions, and personal care.

3. Assign Every Dollar a Job (Hit Zero)

Subtract your total expenses from your total monthly income.

- If you have money left over: Excellent! Now, give it a job. Put it toward building your emergency fund, accelerating your debt payoff, or investing for retirement. You must keep assigning dollars to goals until the remainder is exactly $0.

- If you are in the negative: You have some trimming to do. You will need to reduce your variable expenses or find ways to increase your income until the math perfectly balances at zero.

4. Track and Adjust Throughout the Month

A budget is not a set-it-and-forget-it document; it is a living, breathing blueprint. As the month progresses, track your actual expenses against your planned categories. If you overspend on groceries by $50, you cannot just shrug it off. You must pull that $50 from another category—like dining out or clothing—to keep the budget balanced at zero.

Actionable Tips for Zero-Based Budgeting Success

If you are ready to give every dollar a job, keep these actionable tips in mind to smooth out the learning curve and guarantee your success:

- Create a “Miscellaneous” Buffer Category: Unexpected minor expenses will happen. A forgotten birthday, a minor parking ticket, or a slight increase in a utility bill can derail a tight budget. Assign $50 to $100 to a “Miscellaneous” category to act as a shock absorber.

- Budget for Fun: A zero-based budget is not a prison sentence for your money. If you love buying premium coffee or going to concerts, put it in the budget. Giving yourself permission to spend on things you love (within boundaries) makes the budget sustainable long-term.

- Plan for Non-Monthly Expenses: “Sinking funds” are a zero-based budgeter’s best friend. If you know your car insurance is due in six months and costs $600, assign a job to $100 every month specifically for that future bill. When the bill arrives, the money is already waiting.

- Embrace the 90-Day Learning Curve: Your first zero-based budget will be flawed. You will forget categories and misjudge expenses. That is completely normal. Give yourself three months of practice before you expect to get it perfect.

- Use the Right Tools: While a pen and paper work just fine, digital tools can make the process seamless. Consider using a simple spreadsheet or dedicated zero-based budgeting apps to automate the math and easily track expenses on the go.

Conclusion: Your Wealth Path Starts Here

Transitioning to a zero-based budget requires a fundamental shift in mindset. It moves you from a passive observer of your finances to the active CEO of your money. By sitting down before the month begins and giving every single dollar a job, you eliminate financial waste, accelerate your progress toward your goals, and completely remove the anxiety of the unknown.

Remember, wealth is rarely built by accident. It is built through consistent, intentional habits. Start your zero-based budget today, stick with it through the learning curve, and watch as you finally take total control of your financial destiny.