If you have spent any time on social media recently, you have likely come across mesmerizing videos of people methodically sliding crisp, colorful bills into clear binder sleeves. It is oddly satisfying to watch, but beyond the aesthetic appeal lies a powerful financial strategy. This phenomenon is called “cash stuffing,” and it is taking the personal finance world by storm.

But is it just a fleeting internet trend, or is it a legitimate way to manage your money?

Here at Wealth Path Daily, we know that finding a budgeting system you can actually stick to is half the battle on the road to financial freedom. Today, we are demystifying the cash stuffing trend, exploring why it works, and showing you exactly how to implement it to take back control of your spending.

What is Cash Stuffing?

At its core, cash stuffing is a modern reimagining of the classic “envelope system” popularized by financial experts decades ago.

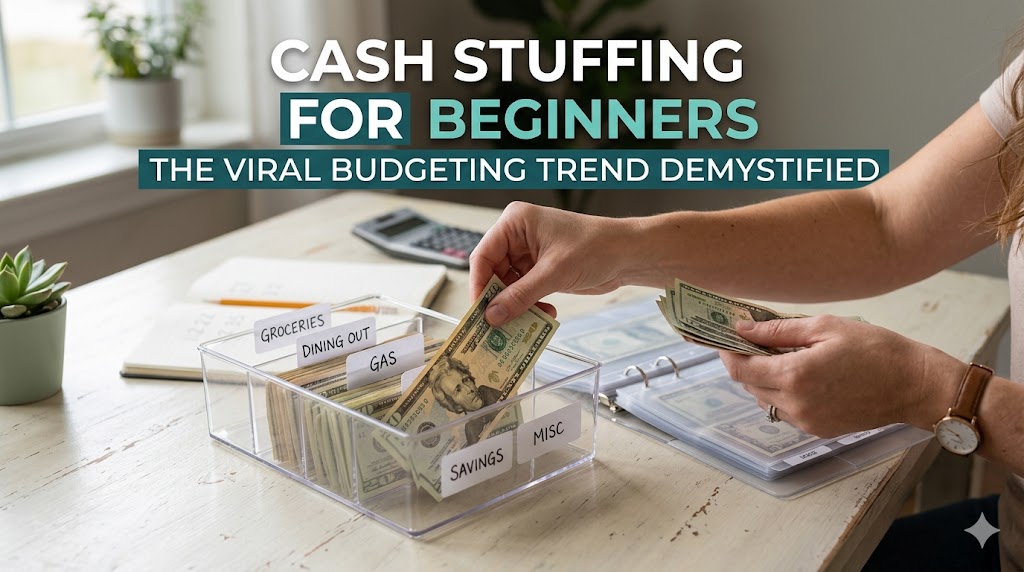

Instead of relying on debit cards, credit cards, and mental math to keep track of your spending, you withdraw your budgeted money in physical cash each payday. You then divide—or “stuff”—that cash into specific envelopes or a dedicated binder. Each envelope is labeled for a different spending category, such as “Groceries,” “Dining Out,” “Gas,” or “Entertainment.”

The fundamental rule of cash stuffing is simple: When the cash in an envelope is gone, you cannot spend any more money in that category until your next payday.

Why is it So Effective?

In an increasingly cashless society, it is dangerously easy to overspend. Swiping a piece of plastic or tapping your phone to a screen feels entirely disconnected from the reality of your hard-earned money.

Cash stuffing works because it introduces friction into your spending. Handing over physical bills triggers a psychological response that a digital transaction simply does not. You physically see and feel your resources depleting, which forces you to pause and evaluate whether a purchase is truly necessary. Furthermore, the visual cue of an empty envelope provides an undeniable, hard boundary on your spending.

How to Start Cash Stuffing in 5 Simple Steps

Ready to give your cards a break and get hands-on with your money? Here is a step-by-step guide to starting your cash stuffing journey.

Step 1: Track Your Current Spending

Before you can determine how much cash to put into your envelopes, you need to know where your money is currently going. Print out your last month’s bank and credit card statements. Highlight and categorize your variable expenses (things that fluctuate, like food, hobbies, and gas). This will give you a realistic baseline to work from.

Step 2: Define Your Cash Categories

Not every bill should be paid in cash. Your fixed expenses—like rent, a mortgage, car payments, and utility bills—should remain securely in your checking account to be paid via direct deposit or online transfer.

Choose to cash-stuff only your variable expenses, as these are the areas where overspending usually happens. Common cash stuffing categories include:

- Groceries

- Dining out and coffee shops

- Gas and transportation

- Personal care (haircuts, cosmetics)

- Entertainment and hobbies

- Miscellaneous/Buffer (for unexpected minor costs)

Step 3: Assign a Dollar Amount (Create Your Budget)

Using the zero-based budgeting method, assign a specific dollar amount to each of your chosen categories for the upcoming pay period. Make sure the total amount you plan to withdraw does not exceed the funds available after your fixed bills and savings goals are met.

Step 4: Head to the Bank and Stuff!

Go to the bank or ATM and withdraw your total budgeted amount in cash. It is highly recommended to ask the teller for specific denominations (e.g., specific amounts of $20s, $10s, and $5s) to make dividing the money easier.

Once you are home, lay out your cash and your envelopes. Methodically stuff the designated amount into each category.

Step 5: Spend, Track, and Adjust

For the rest of the pay period, only use the cash from your envelopes to make purchases in those specific categories. Leave the debit card at home if you have to! At the end of the pay period, evaluate how you did. Did you run out of grocery money too quickly? Did you have leftover entertainment funds? Adjust your budgeted amounts for the next pay period accordingly.

The Pros and Cons of Cash Stuffing

Like any financial strategy, cash stuffing is not entirely flawless. It is important to weigh the benefits against the drawbacks.

The Pros:

- Stops Overspending Instantly: It is mathematically impossible to spend money you do not physically have in the envelope.

- Heightened Awareness: Forces you to be mindful of every single purchase.

- Curbing Impulse Buys: The friction of paying with cash deters unnecessary shopping.

- Debt Reduction: By strictly controlling variable spending, you free up more capital to aggressively pay down debt.

The Cons:

- Security Risks: Carrying large amounts of physical cash can be risky if your wallet or binder is lost or stolen.

- Loss of Credit Card Rewards: You miss out on potential cash-back or travel points (though the money saved from not overspending usually outweighs this).

- Inconvenience: It requires physical trips to the bank and makes online shopping more difficult.

The Hybrid Approach: The Best of Both Worlds

If entirely ditching your debit card feels too extreme, consider a hybrid approach. Many successful budgeters use cash stuffing only for their specific “problem areas.”

If you always stay under budget on groceries but constantly overspend on dining out and clothes, only create cash envelopes for restaurants and apparel. Use your debit card for everything else. This provides the psychological discipline exactly where you need it, without sacrificing the convenience of modern banking.

Conclusion: Take Back Your Financial Power

Cash stuffing is far more than a viral social media aesthetic; it is a proven, tactile method for regaining control over your finances. By pulling your money out of the digital ether and placing it directly into your hands, you create immediate accountability and intention.

Whether you decide to cash-stuff your entire variable budget or just your most problematic spending categories, the result is the same: you give your money boundaries. Try it for a month, embrace the learning curve, and watch as your financial confidence grows. Your wealth path is built one intentional dollar at a time!